Profit slump and financial performance

Tesla’s second-quarter profits for 2024 plummeted by 45%, with net income falling to $1.47 billion, well below analysts’ expectations of $1.9 billion. The electric vehicle giant faced headwinds from slower sales, increased costs due to employee layoffs, and significant investments in artificial intelligence infrastructure.

Despite these challenges, revenues rose 2% to $25.5 billion, narrowly exceeding expectations. This growth was primarily driven by record performance in the energy storage business and an unusually large sum of regulatory credits related to emissions requirements.

Operational costs and margins

Operating expenses soared 39% during the quarter, reaching almost $3 billion. This increase was partly due to restructuring and legal costs associated with the company’s decision to cut 10% of its workforce in April.

Tesla’s gross margin, a closely watched financial metric, fell to 18% in the quarter, down from a peak of 29.1% in the first quarter of 2022. Without the record $890 million in regulatory credit revenues, the automotive gross margin would have dropped to 14.6%.

Strategic focus on autonomy and robotics

Elon Musk, Tesla’s CEO, has shifted the company’s focus towards developing autonomous technologies and robotics. The unveiling of Tesla’s “robotaxis” has been postponed from August to October, with Musk claiming that this project could potentially increase Tesla’s valuation to $5 trillion.

The company is also prioritising the development of Optimus, an autonomous humanoid robot. Musk stated that these robots are already performing tasks in Tesla factories, with limited production for consumer use expected to begin in 2026.

Market position and delivery numbers

Despite the challenges, Tesla delivered nearly 444,000 EVs in the second quarter. While this represents a 4.7% year-over-year decrease, it’s an improvement from the first quarter’s 387,000 deliveries. This performance was sufficient to maintain Tesla’s position as the largest EV company ahead of China’s BYD.

Recent developments and stock performance

Tesla has had an eventful year, with shareholders reapproving Musk’s $56 billion pay award and backing a proposal to reincorporate the company in Texas. Musk has also emerged as a prominent supporter of former president Donald Trump in the upcoming US election.

However, these developments haven’t bolstered investor confidence. Tesla’s stock has fallen 8% in the past 12 months, and its market capitalisation has almost halved from its peak of $1.2 trillion in November 2021.

Company rankings & analyst consensus

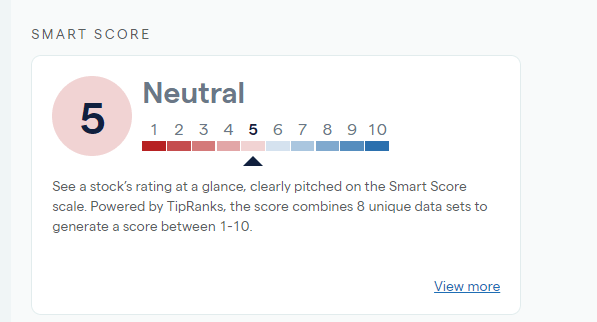

Tesla currently has a neutral rating of 5 on the Smart Score ranking, indicating caution among investors about the outlook.

Source: IG

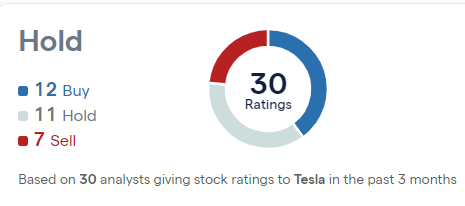

Of 30 analysts currently covering the stock, 12 have ‘buy’ rankings, with 11 ‘holds’ and 7 ‘sells’.

Tesla broker ratings chart

Source: IG

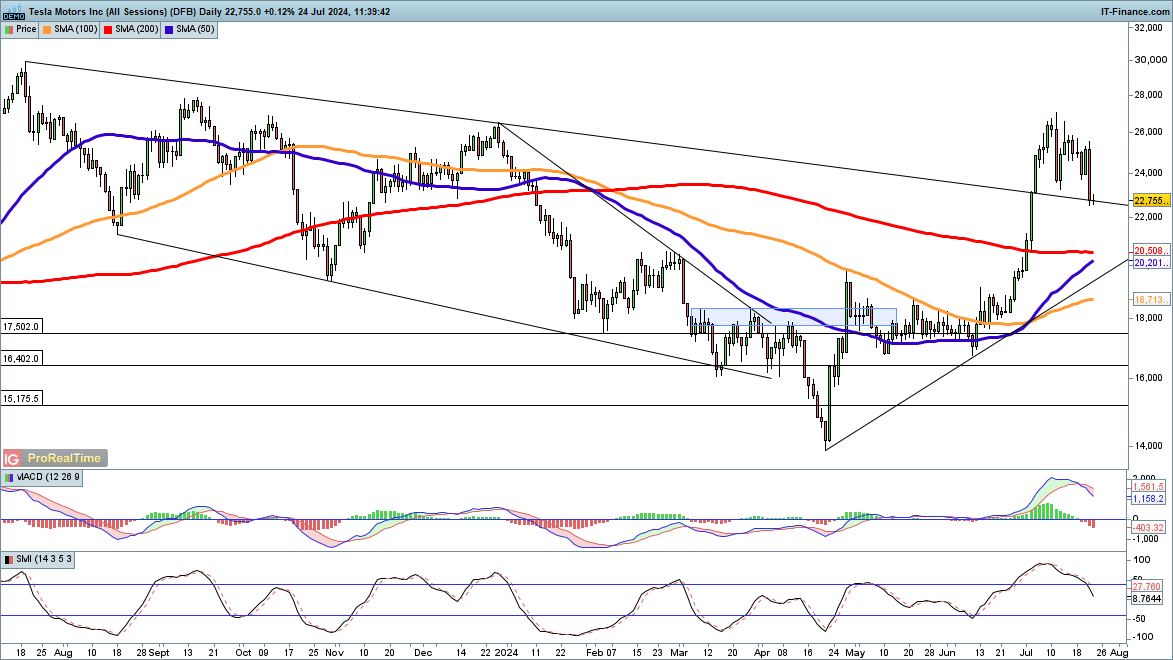

Tesla stock price – technical analysis

The price dropped sharply in the wake of results last night, pushing the stock down 16% from the highs seen earlier in July.

The price is now testing previous trendline resistance from the July 2023 highs, which it broke above around four weeks ago. Tesla has rallied over 60% from the April lows, so some further consolidation or losses would not be surprising.

However, with the 50-day simple moving average (SMA) likely to cross over the 200-day SMA in the near future it appears we could be witnessing a trend change, where dips become buying opportunities.

TSLA chart 240724

Source: IG/ProRealTime

{kind=link}